While inflation still plays a role in Singapore's cost of living in 2025, the residents feel the bite in housing, food, transport, and utilities. When the prices go up and the budget is tight, there is a necessity to weather the economic strain wisely with more astute choices. This handbook provides practical tips to assist Singaporeans in beating inflation, using the current figures and ground-level strategies to support fiscal resilience and lifestyle. Let's look at actionable steps to reduce expenses and stretch your money.

|

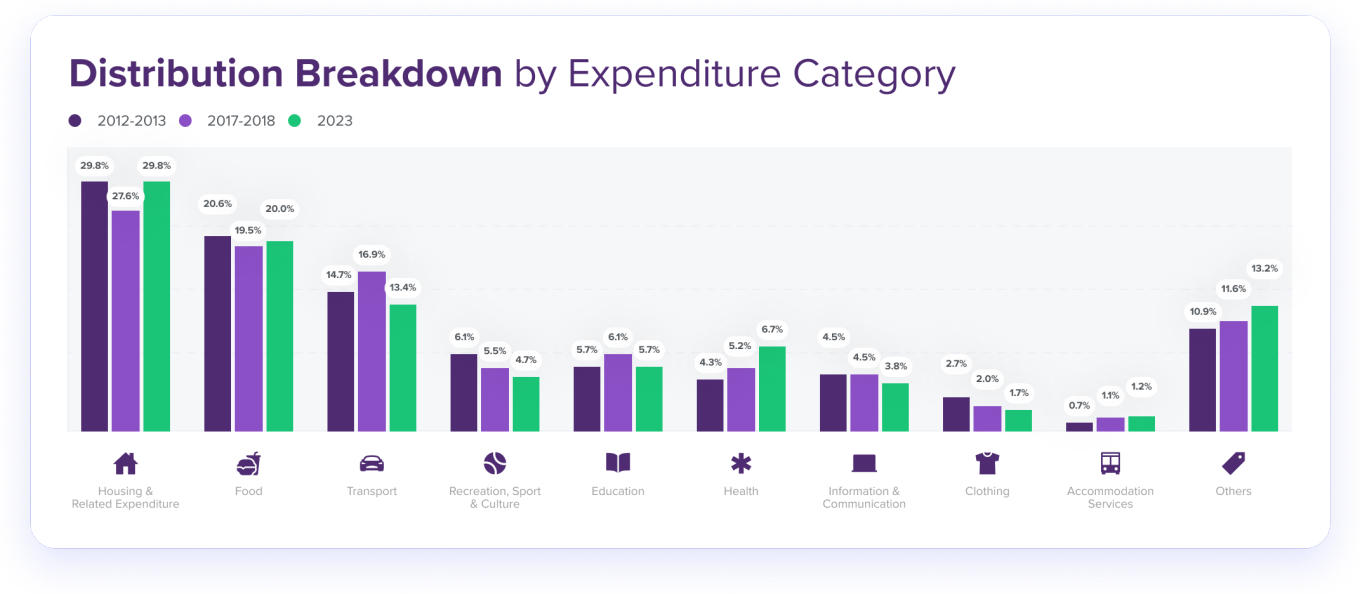

| Figure 1: Distribution Breakdown by Expenditure Category |

1. How Inflation Affects Singaporeans

Daily expenditure has increased due to inflation, and the most expensive item remains housing and utilities at 27.6% in 2023, followed by food at 19.5% and transport at 14.0%, based on recent spending data (see Figure 1). While the numbers show a moderate decline from earlier years, the rise in the price of necessities continues putting pressure on households. By paying attention to necessary areas of expenditure, Singaporeans will be able to spot where they can cut down and adapt to fluctuations in the economy.

2. Reducing Food Expenses through Intelligent Decisions

Food is an expense that can be cut, though, without compromising on nutrition. Capitalize on value options such as food courts, where lunch is $5–$10 compared to restaurants at $15–$25 (see Figure 2). Suppers too can be spared in terms of meal preps or delivery schemes—offers like GrabUnlimited ($5.99/month, saving $45 on delivery charges), Foodpanda Pro ($5.99/month, saving $35–$40), and Deliveroo Plus ($6.9/month, saving $38) provide great discounts on repeat purchases.

|

| Figure 2: Average Food Costs in Singapore |

3. Saving on Transportation

Transportation is where you save as well. Take cost-effective modes such as BlueSG ($0.33/min for short drives), RydePool (20–30% less than normal rides), or Gojek/Grab (25% off peak hours). Riding MRT off-peak hours saves $22 a month, and SimplyGo credit cards give 2% cashback on transport. Multi-transport planning programs also save you $0.30–$0.50 per trip, and you get to drive Singapore's congested roads cost-effectively.

4. Saving on Utility Bills with Energy- and Water-Preserving Solutions

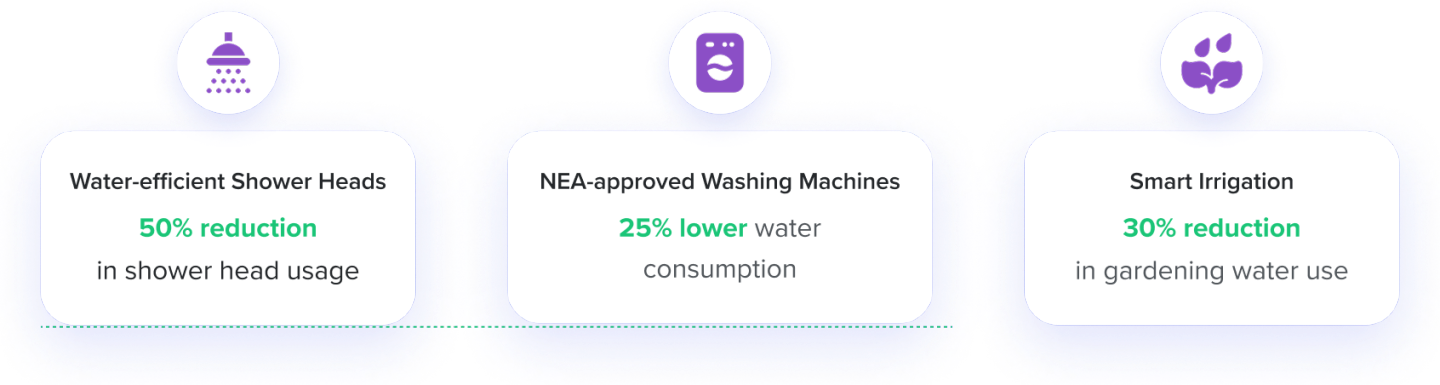

Utilities are an essential expense, but they is technology that can save. Install water-efficient shower heads (50% water savings), NEA-approved washing machines (25% water savings), and smart irrigation systems (30% garden water savings) (see Figure 3). For electricity, enjoy peak vs. off-peak usage ($23.95 cents/kWh savings), smart air-conditioning ($15–25 monthly savings), and LED lighting ($10 monthly savings in the long term after the initial investment). These will cut bills by a considerable amount in an inflationary situation.

|

| Figure 3: Water-Saving Solutions for Singapore Homes |

5. Leverage Discounts and Cashback Promotions

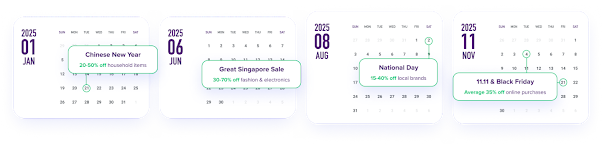

Stretch your wallet during festive promotions. In 2025, buy 20–50% discounts for household items for Chinese New Year (Jan), 30–70% for fashion and electronic items for the Great Singapore Sale (Jun), 15–40% for local brands for National Day (Aug), and 35% for online shopping for 11.11 and Black Friday (Nov) (see Figure 4). Use cashback apps such as Price Kaki (online price comparison in real-time), iPrice (tracking e-commerce sites), and Shopback (average 2.8% cashback), and credit cards such as DBS Live Fresh (5% cashback on online shopping), OCBC 365 (6% for eating out, 3% for groceries), and Citi Cash Back (8% for eating out, groceries).

|

| Figure 4: Major Sales Events in Singapore |

6. Budgeting using Budgeting Apps

Inflation requires budgeting. Utilize low-cost or free budgeting software such as Seedly (free Singapore-specific tracking), Spendee ($2.99/month, multiple currencies supported), and Money Lover ($4.99/month, includes elaborate categorization) to monitor expenditures and areas to save on. These enable you to manage your finances well so that you can effectively respond to increasing costs.

7. Reviewing Investment Options to Overcome Inflation

To invest your money safely, look at Singapore Savings Bonds (3.2% average annual return, $500 minimum investment, government-insured) or retirement saving accounts. For moderate risk, look at corporate government bonds, growth stocks, mutual funds, and bonds. For higher-risk investments, look at real estate, REITs (e.g., CapitaLand Integrated Commercial Trust with 5.8% dividend yield), and stocks, while the riskiest are crypto, day trading, IPOs, and tech stocks (see Figure 5). Invest according to your savings goals and risk tolerance to keep or increase your savings in spite of inflation.

|

| Figure 5: Investment Risk Meter for Singapore |

8. Value for Money Mobile Plans

Pay less for communications through value-for-money mobile plans. Enjoy Zero 1 Starter ($7.06/month, 100GB + unlimited*, Singtel) or VIVIFI Roam Starter ($7.70/month, 100GB, Singtel) for the lowest. Mid-tier plans such as MyRepublic Unlimited ($25.90/month, unlimited, M1) or high-end plans such as Circles.Life 5G Special ($40/month, up to 1TB 5G rollover, M1) cover more needs without breaking the bank.

Conclusion: Surviving Inflation in Singapore

2025 inflation is challenging, but it is manageable with the right measures. By trimming food and transport expenses, lowering electricity bills, taking discounts, budgeting on mobile apps, and investing, you can stay healthy financially. Whether you are a young working individual or a family, these simple tips—grounded on facts and Singaporean insights—can guide you to weather increasing spending while you continue to enjoy Singapore's good living.

This guidebook was first published by ROSHI, the region's top fintech specializing in digital lending solutions. ROSHI empowers Singaporeans with tools and various landing pages such as: https://www.roshi.sg/fast-cash-loan/

No comments:

Post a Comment

Please Leave a Comment to show some Love ~ Thanks